Global semiconductor sales continued to decline in the first quarter, but monthly sales rebounded

"Global semiconductor sales continued to decline in the first quarter of 2023 due to cyclical markets and macroeconomic headwinds, but monthly sales rose in March for the first time in nearly a year, providing optimism for a rebound in the months ahead," said John Neuffer, SIA President and CEO.

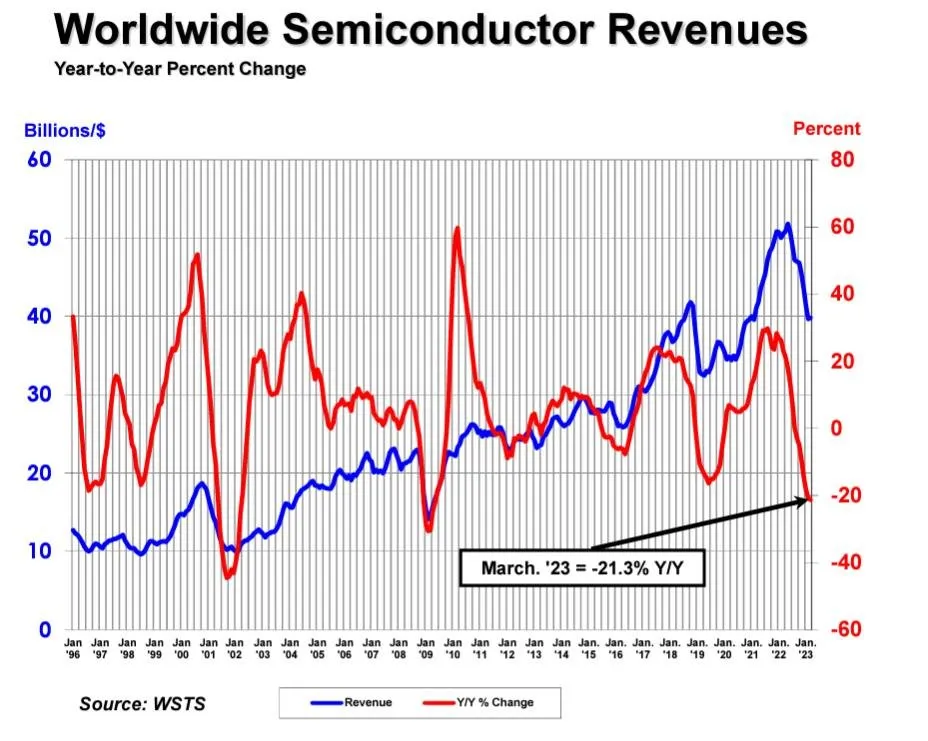

Global semiconductor sales totaled $119.5 billion in the first quarter of 2023, down 8.7% from the fourth quarter of 2022 and 21.3% from the first quarter of 2022, according to a recent report by the Semiconductor Industry Association (SIA). Sales rose 0.3 percent in March compared with February 2023.

By region, March semiconductor sales in Europe, Asia Pacific/All Other regions and China increased by 2.7%, 2.6% and 1.2%, respectively, but semiconductor sales in Japan and the Americas decreased by -1.1% and -3.5%, respectively. Europe, Japan, the Americas, Asia Pacific/All Other Countries and China (-34.1%) experienced year-on-year declines in semiconductor sales, with growth rates of -0.7%, -1.3%, -16.4%, -22.2% and -34.1%, respectively.

"Global semiconductor sales continued to decline in the first quarter of 2023 due to cyclical markets and macroeconomic headwinds, but monthly sales rose in March for the first time in nearly a year, providing optimism for a rebound in the months ahead," said John Neuffer, SIA President and CEO.

According to the figures released by SIA, in February this year, semiconductor sales in Japan increased slightly to 1.2% year on year, but Europe, the Americas, Asia Pacific/all other regions and China showed varying degrees of decline, growth of -0.9%, -14.8%, -22.1%, -34.2%. Monthly sales declined in Europe, Japan, Asia-Pacific/All Other, the Americas and China, with growth rates of -0.3%, -0.3%, -3.6%, -5.3% and -5.9%, respectively.

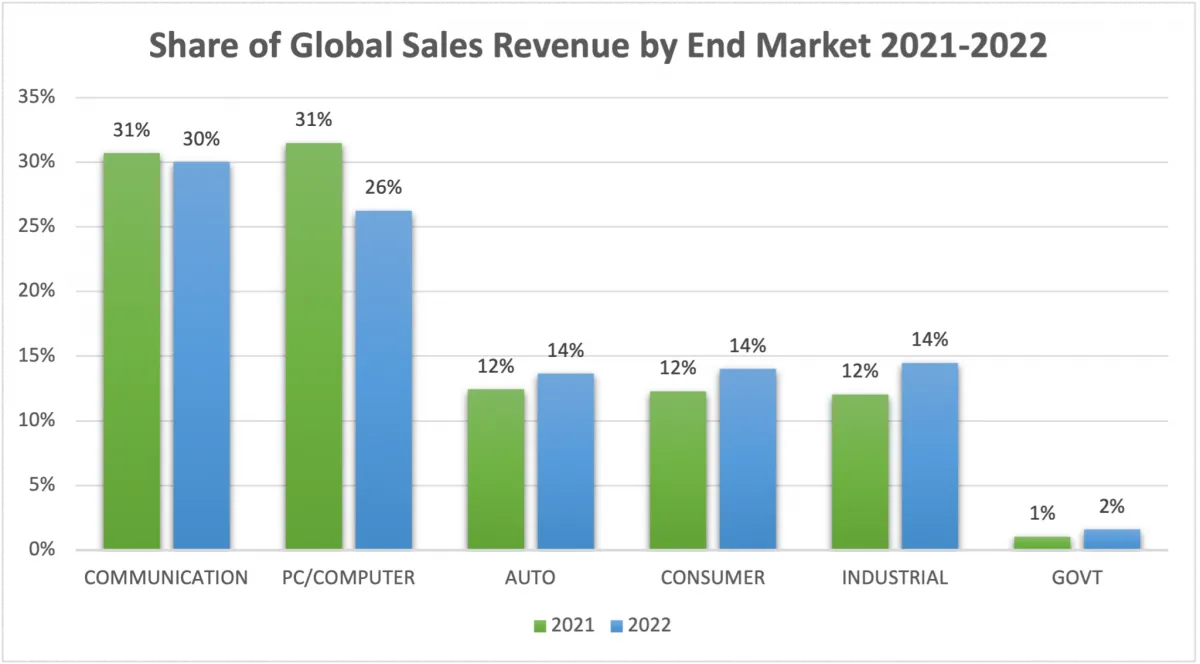

In addition, according to 2022 semiconductor sales data by broad product category (referred to as "end-use"), the PC/ computer and communication terminal markets account for approximately two-thirds of total semiconductor sales, with the other markets being mainly automotive, industrial and consumer electronics.

However, according to the semiconductor end-use survey conducted by World Semiconductor Trade Statistics (WSTS), the semiconductor terminal market saw a significant change in sales in 2022. Although the PC/ computer and communication terminal markets still accounted for the largest share of semiconductor sales in 2022, the lead narrowed. At the same time, automotive and industrial applications saw the largest growth for the year. In addition, automotive and industrial applications will account for 14 percent and 12 percent of average chip sales growth by 2030, respectively, driving demand growth this decade, according to a McKinsey analysis.

Infineon Technologies: Seize low-carbon and digital opportunities, strive to be the

Intellectualization, low carbonization and digitalization are important trends of automobile industry development. Infineon is a global leader in automotive electronics, power systems, IoT and oth…

China has made important breakthroughs in the research and development of 6G communication technology

China has made important breakthroughs in the research and development of 6G communication technology. According to the second Academy of Aerospace Science and Industry, 25 institutes of the Second…

South Korea wants to maintain global dominance and gain a competitive edge in advanced logic chips.

In 2022, there were only five ipos raising more than $100m in the whole year. But analysts believe South Korea's IPO market will gain momentum this year, with a number of companies valued at m…

Will mechanical hard drives end in 2028?

Pure Storage Vice President Shawn Rosemarin recently told the press that HDDS are expected to disappear by 2028 because of the continuing decline in the price of NAND per unit capacity, as well as the…

- Top News

- HRE CSA Series Commercial Grade MLCC Capacitor Selection Guide

- HRE CIA Series Industrial Grade MLCC Capacitor Selection Guide

- HRE CAA/CAI Series Automotive Grade MLCC Capacitor Selection Guide

- FTR20D681K Varistor Applications and Technical Advantages: Providing Comprehensive Protection for Your Circuits

- Samsung Electronics showcases its new automotive technology strategy at Foundry Forum EU 2023