The United States step by step, the local key chip supply strategy how to establish?

The United States has been talking about "de-globalization" and "de-risk", in fact, it wants to kick China away in the context of globalization. Therefore, for China, the most basic and most serious problem is the chip problem.

As an industry highly dependent on global collaboration, the semiconductor industry in recent years due to the epidemic, geopolitical and other multiple factors, resulting in serious damage to the global industrial chain, China's semiconductor industry based on globalization is facing severe challenges. How to build effective strategies to deal with them? How to make good use of China's super-large market, so that partners in the semiconductor global supply chain can benefit together? A series of key questions deserve consideration.

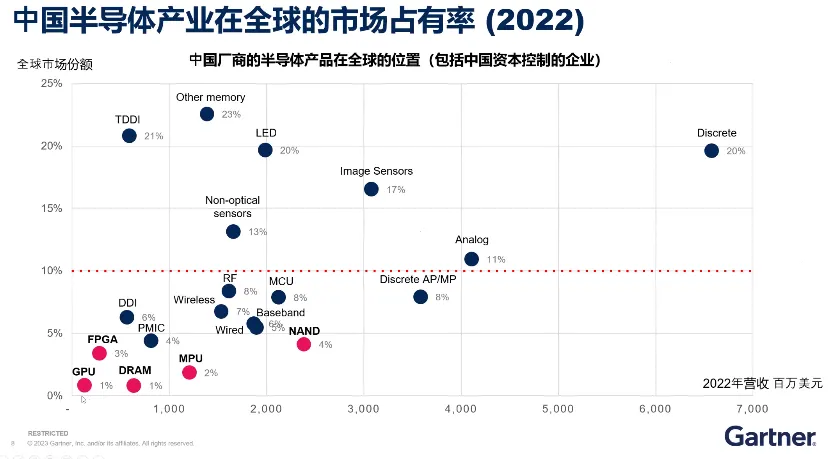

How big is the impact of the US advanced chip embargo on Chinese companies?

At present, we are familiar with the IT infrastructure system, from the bottom computing equipment (servers, PCS), network infrastructure, to the middle layer of operating systems/platforms, cloud services, and then to the top layer of applications, are built on the global unified ecosystem, memory, interface, communication, artificial intelligence applications are also using global unified standards. This also makes the chip the infrastructure that supports the IT industry and digitalization.

However, since the Trump era, in order to contain China's development, the United States has implemented various forms of sanctions and embargoes on China's chip and high-tech industries - from the beginning to include specific Chinese technology companies on the entity list, the so-called "embargo on technology products with more than 5% technology content in the United States", to the implementation of high-performance computing export bans on specific high-performance computing chips; As well as the introduction of advanced chip related export bans, covering all domestic advanced chip manufacturing (including international enterprises' factories in China), and then attracting Allies such as Japan and the Netherlands to implement semiconductor equipment export bans, the intensity and scope are continuing to upgrade.

How to develop chip supply strategy to cope with the future Sino-US competition situation

In order to reverse the unfavorable situation as soon as possible, since the introduction of Trump's policy, the Chinese government has begun to promote the development of the semiconductor industry with greater efforts, including large funds, local funds, science and technology boards, industrial subsidy policies, autonomous and controllable requirements, and a series of support policies including the new national system have been introduced, and local chip manufacturers have also achieved a number of results. For example, process development below 14nm, 3D NAND, mainstream DRAM, independent microprocessors, domestic substitution of mature chips, import of automotive semiconductors, etc., while chip application companies have made breakthroughs in the fields of supplier spare tire strategy, domestic supplier certification, chip design, and independent ecological chain development.

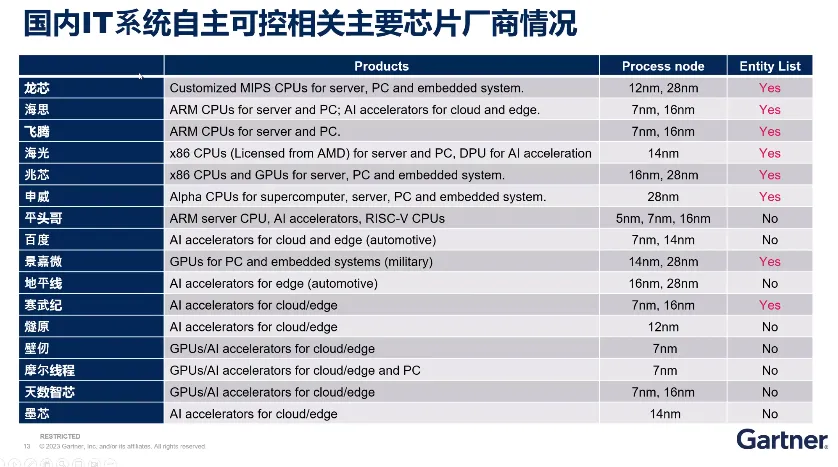

Sheng Linghai stressed the importance of "autonomous and controllable system", believing that IT is a key link to open the entire IT system supply chain. The "IT system supply chain" here covers many fields from core chips and operating systems, to system integration, equipment manufacturing, basic software, storage systems, and then to standard certification, network security, network services, Internet platforms, cloud services, and application software.

"It is only meaningful to integrate application scenarios and suppliers to cultivate the entire ecology through continuous hardware and software running-in." 'he said.

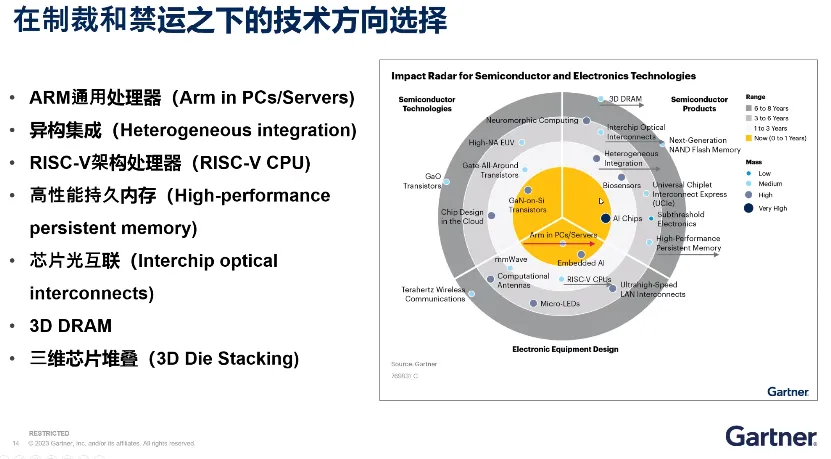

On the other hand, the choice of technical direction under sanctions and embargoes is also very important, especially in the case of high-end advanced processes being "stuck", how to do software optimization, chip-level innovation, and finding specific applications is very critical. The following is the "impact radar map" of the "semiconductor" and "electronics" industries, and Gartner has selected some technology directions that are likely to break the ban and achieve results: ARM universal processors, heterogeneous integration, RISC-V architecture processors, high-performance persistent memory, chip optical interconnection, 3D DRAM, and three-dimensional chip stacking.

Sheng Linghai pointed out that there are three different ways for chip companies to build their own chip capabilities and the scale of investment needed: 1. Strengthen cooperation with domestic reliable chip manufacturers; 2. Invest in potential chip design companies; 3. Self-built chip design and related teams. But each approach also has its own disadvantages, for example, how to judge the priority of cooperation in the first mode? In the second model, should we distinguish between financial investment and strategic investment? The third model requires a lot of capital and manpower investment, etc., and needs to be carefully discussed for different products and fields, and then decide the direction.

He hopes that domestic semiconductor chip manufacturers, electronic equipment manufacturers, cloud infrastructure service providers and digital businesses can "establish a domestic development ecosystem through upstream and downstream collaboration in the industrial chain" and empower each other. After all, building your own ecosystem is a very difficult thing, and for many chip startups, it is unrealistic to expect a chip to "kick Nvidia and punch AMD" right away.

To this end, Shenglinghai put forward the following six points as alternative action suggestions for the establishment of domestic IT systems:

Collaborate with IT systems supply chain vendors to study and predict the impact of U.S. sanctions that have occurred and may occur in the future.

Select domestic autonomous controllable related systems and chip manufacturers to confirm the existing product status and market practical application experience, and establish cooperative relations.

Set reasonable performance requirements and verification purposes for domestic systems and chips, and try to import some domestic IT systems from non-critical applications.

Strengthen software adaptation development to ensure software compatibility, stability and operational performance for different systems.

Establish or strengthen investment in domestic basic IT hardware and software vendors to ensure influence on their product development plans.

When establishing a new product development program, prioritize domestic supply chains and mature platforms, and actively adopt semiconductor innovation technologies.

When asked whether the chip industry will recover in 2024, Sheng Linghai said, "Yes, but to what extent it can recover depends on many factors, such as the Russia-Ukraine war, the degree of inventory digestion in the market, the U.S. presidential election and so on." As for whether the growth rate of China's chip industry can exceed that of the world, it depends on whether mobile phones, automobiles, and industrial chips can achieve higher growth rates.

He predicted that in the next five years, the use of 28nm, 40nm process of local network chips, consumer chips, MCU, automotive chips, analog chips will gain rapid growth. The current hot speculation of "big computing chip", although the long-term trend is good, but if it does not completely solve the high technical threshold, flow sheet supply chain and other problems, it will still be a long-term exploration process.

Will mechanical hard drives end in 2028?

Pure Storage Vice President Shawn Rosemarin recently told the press that HDDS are expected to disappear by 2028 because of the continuing decline in the price of NAND per unit capacity, as well as the…

South Korea wants to maintain global dominance and gain a competitive edge in advanced logic chips.

In 2022, there were only five ipos raising more than $100m in the whole year. But analysts believe South Korea's IPO market will gain momentum this year, with a number of companies valued at m…

What are domestic chip manufacturers doing with the rapid landing of large models?

The turning point for 2022-2023 has arrivedWhat is the turning point for 2022-2023? It is the emergence of the AI big model that has turned the marginal cost of acquiring knowledge into a fixed cost. …

What are the latest developments in SiC and GaN 'boarding'?

Although SiC has been widely used in automobiles, the cost of SiC devices is still too high for most cars due to yield and cost-effectiveness issues; The commercial use of GaN is concentrated in the f…

- Top News

- HRE CSA Series Commercial Grade MLCC Capacitor Selection Guide

- HRE CIA Series Industrial Grade MLCC Capacitor Selection Guide

- HRE CAA/CAI Series Automotive Grade MLCC Capacitor Selection Guide

- FTR20D681K Varistor Applications and Technical Advantages: Providing Comprehensive Protection for Your Circuits

- Samsung Electronics showcases its new automotive technology strategy at Foundry Forum EU 2023